Import of Medicinal and Investigational Medicinal Products into the European Union

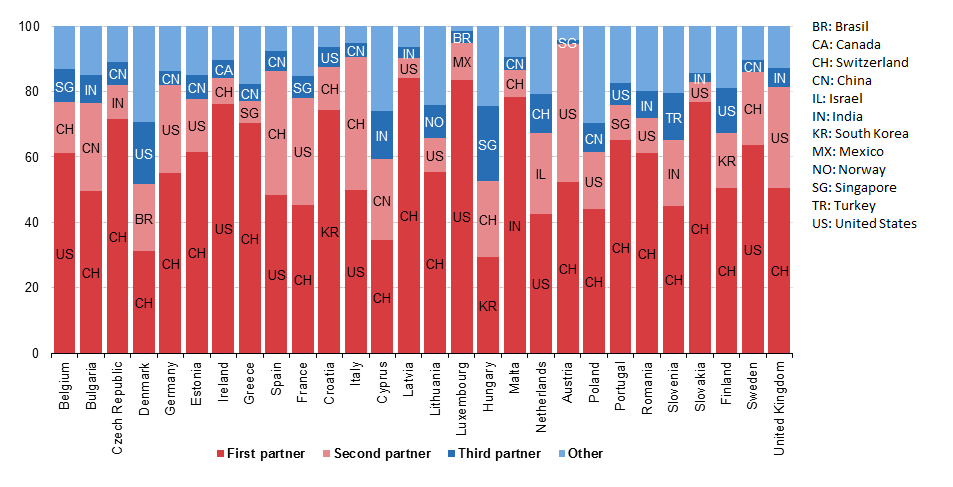

The European Union is a large importer of medicinal and pharmaceutical products. Its main trading partners are the United States and Switzerland but also Brazil, China, Israel, India, South Korea, Mexico, Norway, Singapore and Turkey showed strong presence in 2016.

Source: Eurostat: International trade in medicinal and pharmaceutical products 2016

Challenges of an EU Import

The major challenges for import activities into the EU are related to

- Customs clearance (how to determine appropriate customs procedures)

- Taxes / VAT (how to legally avoid import turnover taxes, how to optimize cash situation)

- Legal aspects (how to deal with import permissions, how to get batches certified by a Qualified Person and released to the EU market)

Target for deliveries to the EU: Implement a full service situation

- Get the legally required activities regarding EU import, batch certification and EU Release of the drug products properly executed

- Get the handling of import turnover taxes and customs duties optimized, secure tax-free deliveries to the final EU recipients, optimize your cash situation, use a fiscal representative

- Get appropriate customs procedures established for each individual situation

- Take advantage of a highly professional logistics service organization providing you with the needed logistics services

Customs clearance & Fiscal representation services

The fiscal representative takes over the all duties with regard to VAT, customs and INTRASTAT filing. The foreign company can enter the EU market without worrying on customs, statistical and VAT regulations, it’s made sure the company is 100% compliant!

- No VAT registration necessary

- Higher degree of compliance, the fiscal representative takes care of all requirements

- Foreign company can concentrate on its core business

- Consignee receives goods as intra-Community delivery, no additional activities required at place of destination

- No expertise on EU customs, VAT and statistical legislation required

- Cash flow advantage due to payment of VAT at the place of destination

Bonded warehouse

Owner of the goods has not to pay any duty until the goods are sold or shipped.

- Customs duties incl. import turnover taxes are suspended / deferred und until goods are released for free circulation

- Cost items become due upon actual sale within the EU or further dispatch to other EU destination(s) (Credit function – cash conservation, interest gain)

- In case non-EU goods will should be delivered to an EU third country no cost items become due and trade measures (e.g. import permissions) are suspended (Transit function)